The most widely-read article on this blog these days one that I wrote two years ago called The Myth of DRM-Free Music. So I thought I’d follow up on it.

I wrote that piece as a reaction to the popular story — which was coursing around the book publishing industry at the time — that Apple led the music industry away from DRM when iTunes went entirely DRM-free in January 2009. This story was a myth, on two levels.

On the more superficial level, this story was one of the more enduring creations of the legendary Steve Jobs Reality Distortion Field. Long before Apple’s iTunes announcement, there had been rumblings within the music industry about the major labels’ desire to find viable competitors to Apple, and their willingness to give up DRM in order to promote interoperability beyond Apple’s iTunes/iPod/iPhone walled garden. Amazon emerged as the entity that could credibly compete with Apple, and it became evident that the majors were working on deals that would enable Amazon to sell DRM-free MP3s. Steve Jobs heard the rumblings and decided to “get in front of the train” by putting out his now-famous 2007 “Thoughts on Music” open letter and positioning himself as the white knight who led the music industry away from DRM. This view of Jobs’s PR opportunism was confirmed as recently as 2012 by an engineer who helped develop the DRM for iTunes.

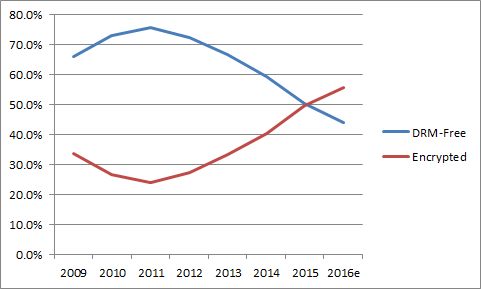

On a deeper level, the myth was that DRM really went away from music at all. David Hughes, Chief Technology Officer of the RIAA, liked to say that there were many ways of distributing digital music, and all of them used some form of DRM except one: paid permanent downloads. Those of us who heard this treated it as little more than a rhetorical flourish. But since sometime last year, it has taken on a new meaning: music delivered with some form of encryption now earns more total revenue than music delivered DRM-free.

My article in May 2015 predicted that “encrypted modalities will represent the majority of recorded digital music revenue by 2016.” This wasn’t exactly rocket science, given the graph that showed two lines — percentages of digital music revenue delivered with and without encryption — converging towards each other. But now it has actually happened:

Percentage of recorded music industry digital revenue from DRM-free vs. encrypted delivery modalities. Sources: RIAA, Pandora Media, Sirius XM Radio.

Note that this chart is not exactly an extension of the one from two years ago. On that chart, I counted a fixed portion of digital radio revenues (SoundExchange distributions), on the basis that such a percentage comes from services that encrypt their signals. This time I got more accurate about that calculation.

SoundExchange collects digital performance royalties on five types of services: pure-play Internet radio (e.g., Pandora), AM/FM simulcasts (iHeartRadio), satellite radio (Sirius XM), cable/satellite TV radio (Music Choice), and business establishment music services (Muzak, DMX). Most of these services encrypt their signals, the primary exception being many AM/FM Internet simulcasts. Unfortunately, SoundExchange doesn’t break out its collections (revenue) by service type, so we have to do some calculations to estimate what percentage of its revenue comes from encrypted sources.

As it turns out, two services that encrypt their signals account for the vast majority (75-90%) of SoundExchange’s collections: Sirius XM and Pandora. Both are publicly traded companies, so it’s possible to get a good idea of how much they pay SoundExchange from their annual reports. In Sirius XM’s case, they pay SoundExchange a percentage of their annual revenues that is set by law (and varies from year to year). Pandora’s rates are also set by law and are more complicated, but Pandora does us the favor of reporting how much of its revenue it pays to SoundExchange in its annual reports. (Neither Sirius XM nor Pandora pay royalties to SoundExchange on recordings either made before 1972 or on labels that have direct licensing deals with the service.)

In the above graph, I’ve taken the percent of revenue that SoundExchange gets from Sirius XM and Pandora and applied that percentage to the amounts that it actually distributes to record labels, i.e., the figures that it reports to the RIAA. The result is a good estimate — a tight lower bound — of the percentage of SoundExchange distributions that come from encrypted delivery channels.

Apart from SoundExchange, assigning recorded music revenue sources to encrypted and DRM-free buckets is straightforward. “Paid Subscriptions” (e.g., Spotify Premium, Apple Music, Pandora One) and “On Demand Streaming (Ad-Supported)” services (e.g., Spotify Free, YouTube) are encrypted, while downloads are DRM-free. I treat “Ringtones & Ringbacks” as encrypted, even though some probably aren’t, and in any case that revenue source has shrunk into insignificance (now less than 1% of total recorded music revenue) so it’s not material.

The fact is that sometime during 2015, digital music with some sort of encryption scheme became bigger than DRM-free — by consumer choice. Sales of downloads have been dropping since 2013 and are now essentially in free fall, while all forms of streaming and subscription downloads (a/k/a “offline listening mode”) are on the rise. This relates to the point I made recently about how consumers don’t seem to value ownership of pure digital files very much. Certainly this is the case in book publishing, where e-book sales are stuck below 25% of trade book sales despite all the breathless predictions of the late 2000s that e-books would exceed print books by now.

The big difference between books and music in this respect — as my colleague Mike Shatzkin pointed out — is that while there’s a big difference in the user’s experience of the actual content between print books and e-books, there’s very little difference between the user’s experience of recorded music between physical and digital media. That helps explain why print books outsell e-books by more than 3 to 1, while for vinyl and digital music it’s the other way around.

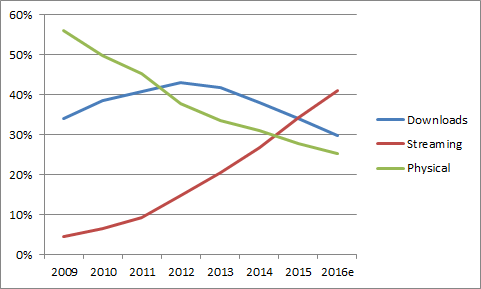

At the same time, physical music products — including CDs, which are physical digital products — seem to be finding a floor. In addition to the well-known rebirth of vinyl LP sales, the decline in CD sales has slowed down, and cassettes are even starting to make a comeback thanks to their lower cost and faster turnaround time to produce.

Percentage of recorded music revenue from downloads, streaming, and physical products. “Streaming” includes subscription downloads. Source: RIAA.

This chart suggests that physical music products may bottom out around 20% of total industry revenue. We’ll know more next month when the RIAA releases its revenue figures for the second half of 2016.

[…] Source: The Myth of DRM-Free Music, Revisited | Copyright and Technology […]

Nice work Bill. I should add, ALL of the streaming music services use DRM esp the ones with downloads 🙂

Actually that is not quite true. I just checked it carefully.

First, “Streaming” covers a lot of territory. Interactive streaming (Spotify, Apple Music, Google Play, Rhapsody, Deezer, Tidal) – yes, definitely all encrypted. Satellite radio (Sirius XM), yes, also encrypted. And business establishment services like Muzak and DMX probably also encrypt because they are also paid subscription services. But so-called noninteractive streaming varies. It’s possible that pure-play Internet radio services such as Pandora encrypt their signals; I don’t know for sure, and they ain’t tellin’. On the other hand, AM/FM simulcast signals generally don’t encrypt; anyone can use a standard stream recorder and capture those signals. These signals are available through individual station apps and through aggregators such as TuneIn and the NPR app.

Then there’s the problem of assigning recorded music revenue to each of those types. Interactive streaming services get broken out by the RIAA numbers pretty cleanly. Digital radio services with statutory licenses that pay royalties through SoundExchange are the problem. SoundExchange does not break out its royalty collections by type of service. It’s not possible to tell how much of SoundExchange’s revenue comes from pure-play webcasting (Pandora and its ilk), because Internet radio (noninteractive webcasting) royalties are calculated on a per-stream basis and not as a percentage of revenue, and that data’s not available. It’s not possible to tell how much of SoundExchange’s revenue comes from business establishment services because the largest one, Mood Media (owner of Muzak and DMX), offers various other non-royaltable services and doesn’t break out its revenue.

The only one we can tell with any accuracy is satellite radio, which we know is encrypted and which actually brings in more than half of SoundExchange’s revenues, so it’s a decent lower bound. We can tell how much Sirius XM satellite radio pays to SoundExchange by taking advantage of the fact that it’s the only satellite radio (SDARS) service and using publicly available data on its revenues and its statutory digital performance royalty rates. From there we can calculate the percentage of SoundExchange revenue that comes from satellite radio. So I’m using that as a lower bound for the percentage of revenue to assign to the “Encrypted” category; the true number is somewhat higher.

In other words, it’s possible that the true crossover point was up to a year earlier than 2016, but still recent.

The other problem with these figures in general is that they only count recorded music revenues. They don’t count revenues from music publishing (performance and mechanical royalties collected by the likes of ASCAP, BMI, Harry Fox, and major music publishers). Total U.S. music publishing revenue is about 30% of recorded music revenue, though a) that’s rising slightly each year, b) the royalty rates are completely different from those of recorded music, like apples and oranges, and c) the music publishing industry (represented by the NMPA) doesn’t break out revenues the way the RIAA does for recorded music — all of which makes it impossible to calculate for these purposes.

“digital music with some sort of encryption scheme became bigger than DRM-free — by consumer choice. ”

Is it fair to describe this as “by consumer choice” if consumers are not properly informed?

Ok, I’ll bite: informed about what?

I am one of those “rare” consumers who wants her entire mp3 music library (that she already owns) to be able to be played on any device or through whichever app she chooses. If I pay for it, it should be MINE!

This streaming business model leaves those of us with unreliable phone reception and a desire for spur of the moment track play completely out in the cold. Even using Google play as my music player phone app requires me to “download” the music I already own just so i can play it through their player. Why must I repeatedly “download” the music I already have on my sd card? It’s a really terrible system that we’ve moved into. Amazon music player now doesn’t allow you to play music that you purchased from any other platform. So stupid!

I’m only 35 but completely geriatric in terms of how I want my music, I guess. What are the chances of this ever getting reversed? Anyone know of any reputable sites where I can legally buy mp3’s without digital restrictions?

Julie,

There are ways to do what you want. But first, I think you should understand the differences between what you are *legally entitled* to do with your MP3 and what the various music platforms *enable you to do* with them.

tl;dr version: use an independent MP3 player app with cloud sync capability like DoubleTwist, BlackPlayer, EverMusic, or CloudPlayer instead of Amazon’s or Google’s or Apple’s. Which one you pick depends on which devices you have, since some of them are iOS only, some are Android only, and some are bilingual.

Otherwise, this is a quintessential example of how tech companies can construct walled gardens without DRM.

In terms of what you’re legally allowed to do: there are two sources of legal authority here. One is copyright law; the other is the license agreement with the place where you got your MP3s. Copyright law says it’s probably OK for you to use your MP3s on any of your personal devices, which means making copies of them for each device. So, for example, if you ripped your own CD, you’re most likely within your rights under US law to make copies of the resulting MP3 for each of your devices for your personal use. On the other hand, if you got your MP3s from iTunes or Amazon, then technically you need to abide by the terms in their terms of use, and copyright law doesn’t apply. But the terms of use (at least Amazon’s, which I just looked at) suggest that it’s OK to do what you want to do with MP3s purchased on the retailer’s site, as long as it’s for personal, noncommercial use. In neither case is it OK to do things like resell the files or give them away, which you could do with physical objects like CDs. There are no true ownership rights on MP3 files in US copyright law.

Now in terms of what the platforms enable you to do: Amazon’s scheme for restricting its player app to files purchased on Amazon (or obtained through its CD AutoRip program) is probably based on some header data that it puts into its files. If it finds valid header data, it will play the file; if it doesn’t find it, it won’t. You could fake that header data in other files if you wanted to, so that they will play in the Amazon player. But that would be a needless waste of time.

Instead, if you have a lot of MP3s that you didn’t buy on Amazon, you should try an independent music player app with cloud sync capabilities, such as DoubleTwist, BlackPlayer, Evermusic, or CloudPlayer (there are many of them, just search “cloud music player app”). It depends primarily on which type(s) of devices you own (iOS, Android, Mac, Windows). Any of these should work with all your MP3 files regardless of where you got them. I’m guessing they have setup processes that look for files purchased on iTunes, Amazon, Google, and possibly other retailers.

Bill,

I was definitely in the market for a new media player app. Thank you so much for your recommendations! I have an Android phone and have been only on Android since springing my music from iTunes over a decade ago made choosing an iPhone seem silly.

I’m happy to purchase music off Amazon as long as I can play it on several platforms. I’m curious as to the best (and most automatic) way to move purchased music from Amazon immediately into a media player app on my phone.

Would any of the cloud media players be able to play Amazon mp3s directly from my phone after I’ve downloaded them from the Amazon phone app? That may seem like a stupid question, but when you literally can’t do that with Google play and the pulsar music app I just downloaded, I’m doubting the possibility without involving my laptop.

Thanks again for the reply, Bill. I would’ve replied sooner but December is crazy!

[…] 그림 8. 디지털 음악 시장의 콘텐츠 유형별 매출 비중 (참고 2) […]

[…] Figure 8. Sales portion of digital music market by content type (ref 2) […]

[…] Video Streaming Now Makes Up 58% of Internet Usage Worldwide 2. The Myth of DRM-Free Music, Revisited 3. PallyCon Multi-DRM Cloud on AWS Market […]

[…] Video Streaming Now Makes Up 58% of Internet Usage Worldwide 2. The Myth of DRM-Free Music, Revisited 3. PallyCon Multi-DRM Cloud on AWS Market […]